Method Lab

The Data Gap: Why Bureau Snapshots Miss Refi-Ready Borrowers

/

March 5, 2026

The Data Gap: Why Bureau Snapshots Miss Refi-Ready Borrowers

Priyanshi Churiwala

Product Lead, Lending

Artem Vasilkovskiy

Finance and Business Operations Lead

Table of contents

The Refinance Window Is Open

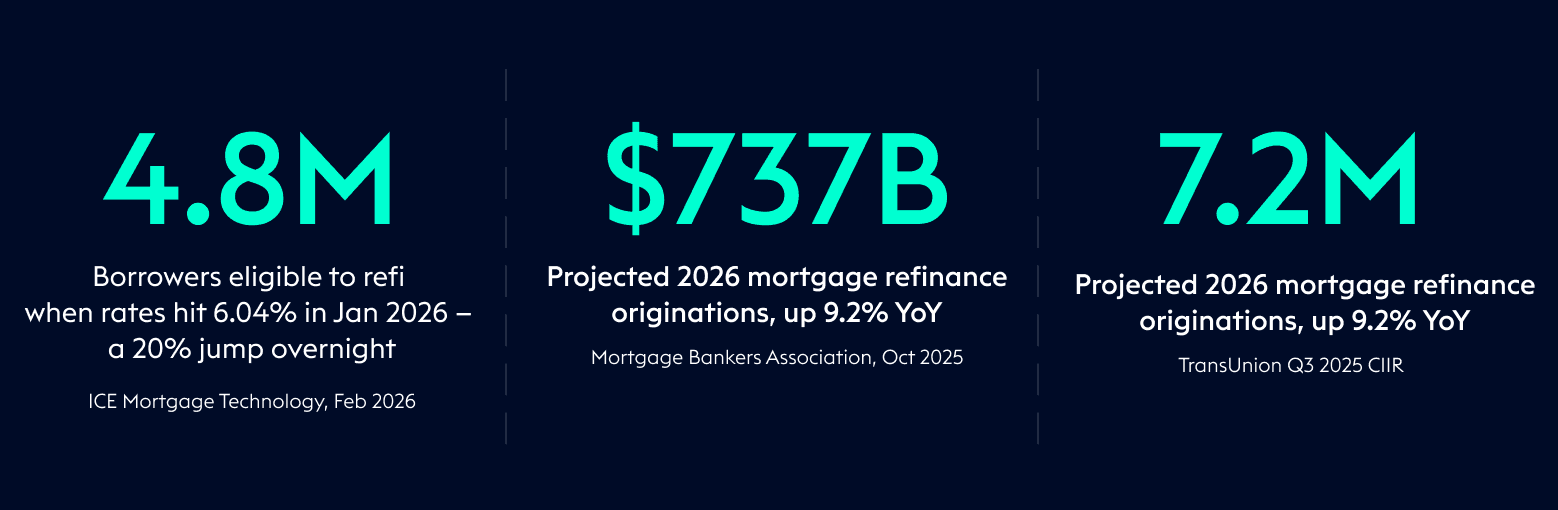

The 30-year fixed mortgage rate averaged 6.01% as of February 19, 2026 — its lowest level since September 2022, down from 6.85% a year prior.¹ The Mortgage Bankers Association forecasts refinance originations will reach $737 billion in 2026, a 9.2% increase over 2025.² Fannie Mae projects the refinance share of total originations will climb from 26% to 35% as rates continue to ease.³

In early January 2026, a brief rate dip to 6.04% expanded the refinance-eligible population by 20%, bringing 4.8 million borrowers into potential qualification — the highest refi-eligible pool since early 2022, per ICE Mortgage Technology.⁴

The personal loan market is moving in parallel. Unsecured personal loan originations hit a record 7.2 million in Q3 2025. TransUnion forecasts personal loan originations will grow 5.7% in 2026, outpacing mortgages, credit cards, and auto loans. Fintech lenders now hold a 42% share of personal loan originations, up from roughly one-third a year prior.⁵

For product, credit risk, and growth leaders inside lending organizations, this raises a more practical question: how accurately are we identifying who is actually refinance-ready today? The answer depends almost entirely on the freshness of the liability data underlying that determination.

How Old Is “Current” Bureau Data?

Lenders rely predominantly on credit bureau snapshots to assess borrower eligibility. These snapshots reflect the balance and status of a consumer’s liabilities at the time of the last furnisher report — typically when a statement cycle closes. By the time a lender pulls a bureau file and evaluates it, a material lag has already accumulated.

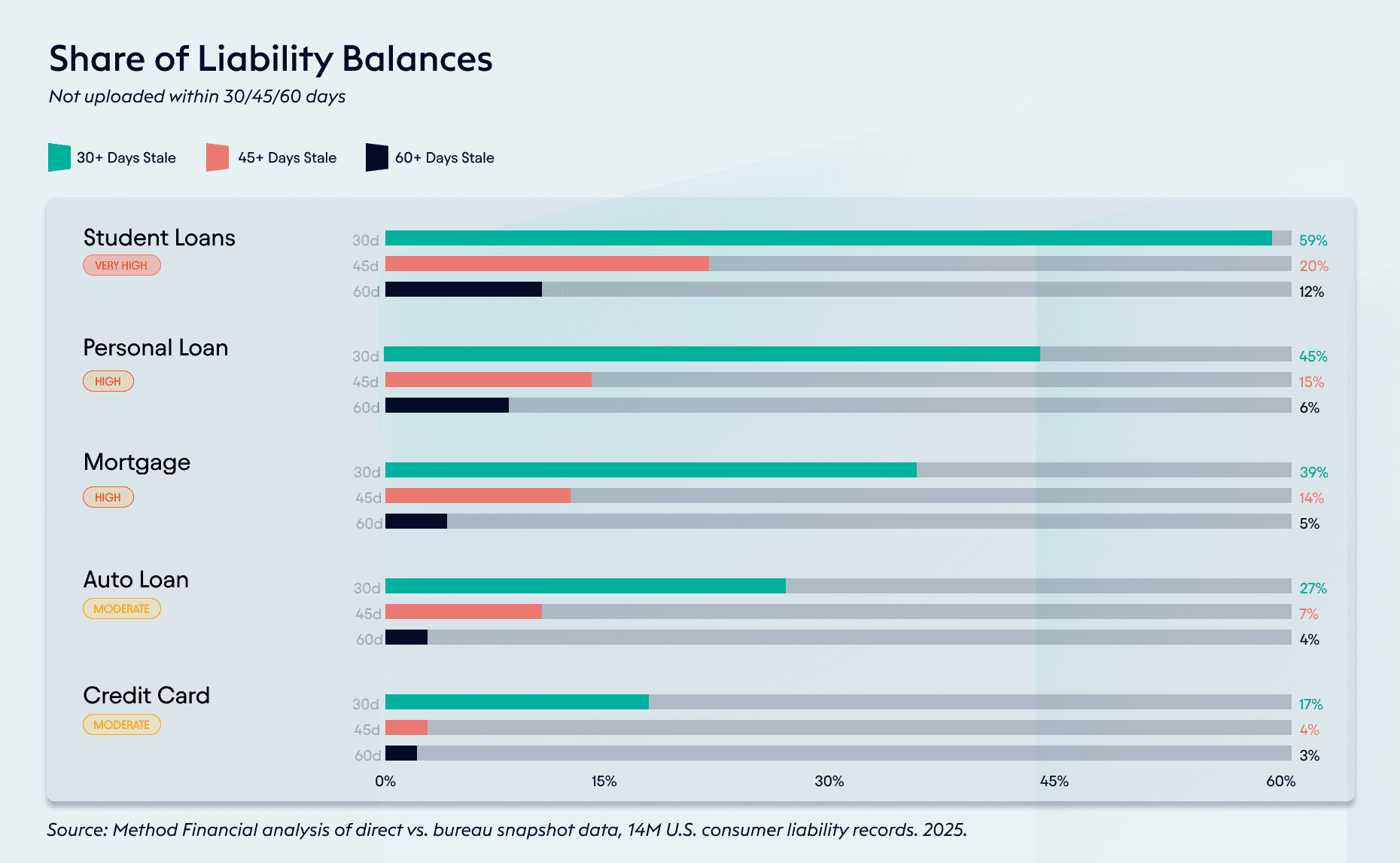

Method’s analysis of real-time liability data against bureau snapshot data, across a base of 14 million U.S. consumers, quantifies this lag by product type.

Student loan data is structurally the most delayed — 59% of snapshots are 30+ days old at time of bureau pull, and 12% are over 60 days stale. Personal loans have 44% of balances updated more than 30 days prior. Mortgage data shows 39% of snapshots at 30+ days. Credit cards update most frequently, but still carry a meaningful lag for 1 in 6 balances.

In an environment where rate windows open and close within weeks, a 30-to-45-day information lag is not a minor inconvenience. It is the difference between reaching a borrower who is currently eligible and missing them entirely.

The Mismeasurement Problem

Data age is one issue. Balance accuracy is another. Even when bureau data is relatively recent, the balance it reports may diverge materially from a borrower’s actual current balance — because the bureau reflects statement-date balances, not real-time account balances. Payments made after a statement closes are invisible until the next reporting cycle.

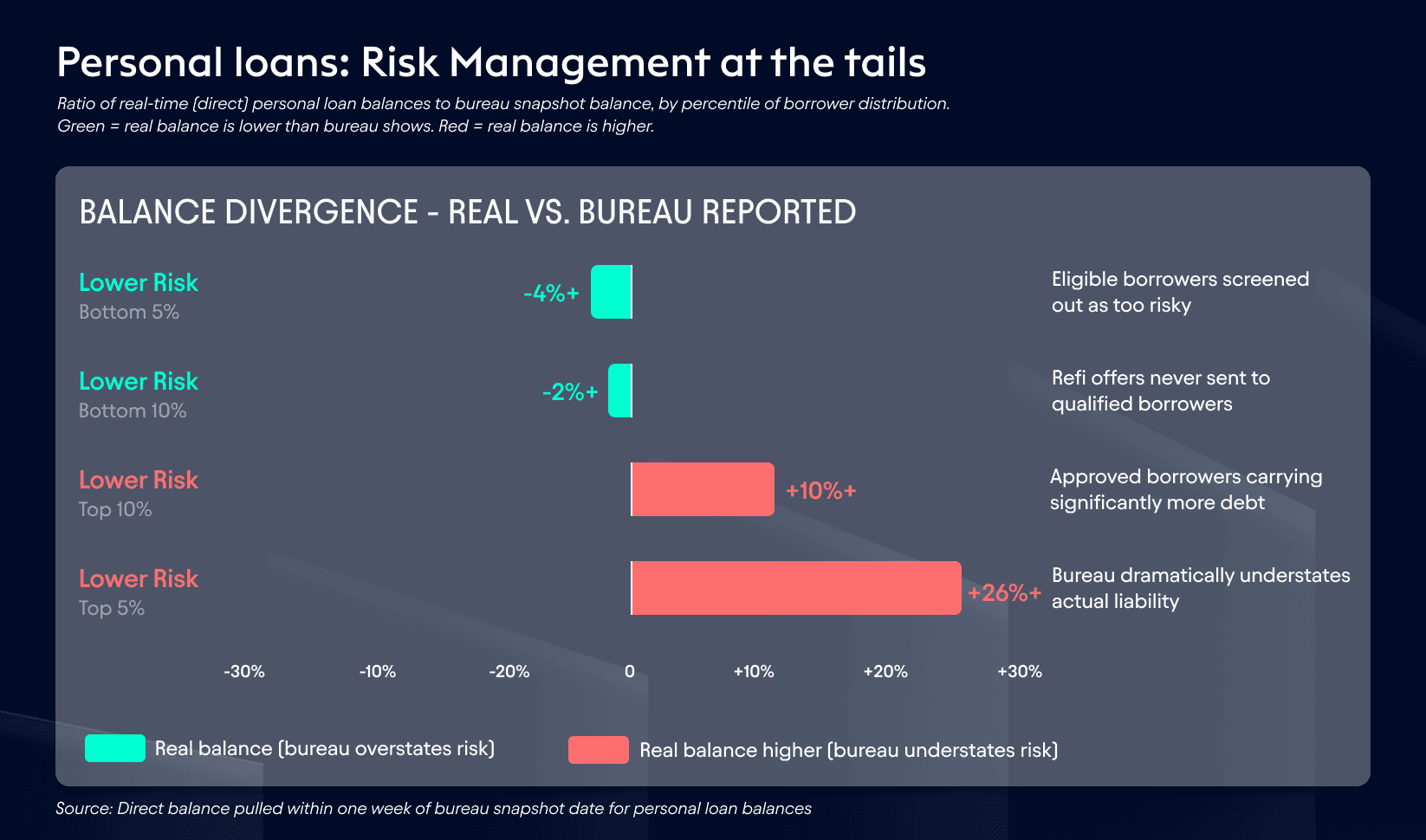

Method compared its real-time “direct” balance reads against the most current bureau snapshot balance for the same accounts, across product types. The ratio of direct-to-snapshot balances was examined across the full distribution of borrowers. The tails reveal the practical consequences for lenders.

For borrowers at the upper tail of the distribution, the error runs in the opposite direction: bureau data can understate the borrower’s actual liability load. In Method’s analysis, borrowers in the top 10% of the distribution carried real balances more than 10% higher than what bureau snapshots reflected, with the top 5% exceeding 26%.

For lenders, this means some borrowers appear safer than they actually are at the time of decisioning. Approvals issued using snapshot balances may therefore be based on materially understated liabilities, leading to risk profiles that differ from what underwriting models assumed.

For lenders operating on thin unit economics, even small shifts in approval accuracy compound quickly. A portfolio where a portion of approved borrowers carry meaningfully higher real balances than reported is not simply a modeling artifact — it is a structural risk exposure

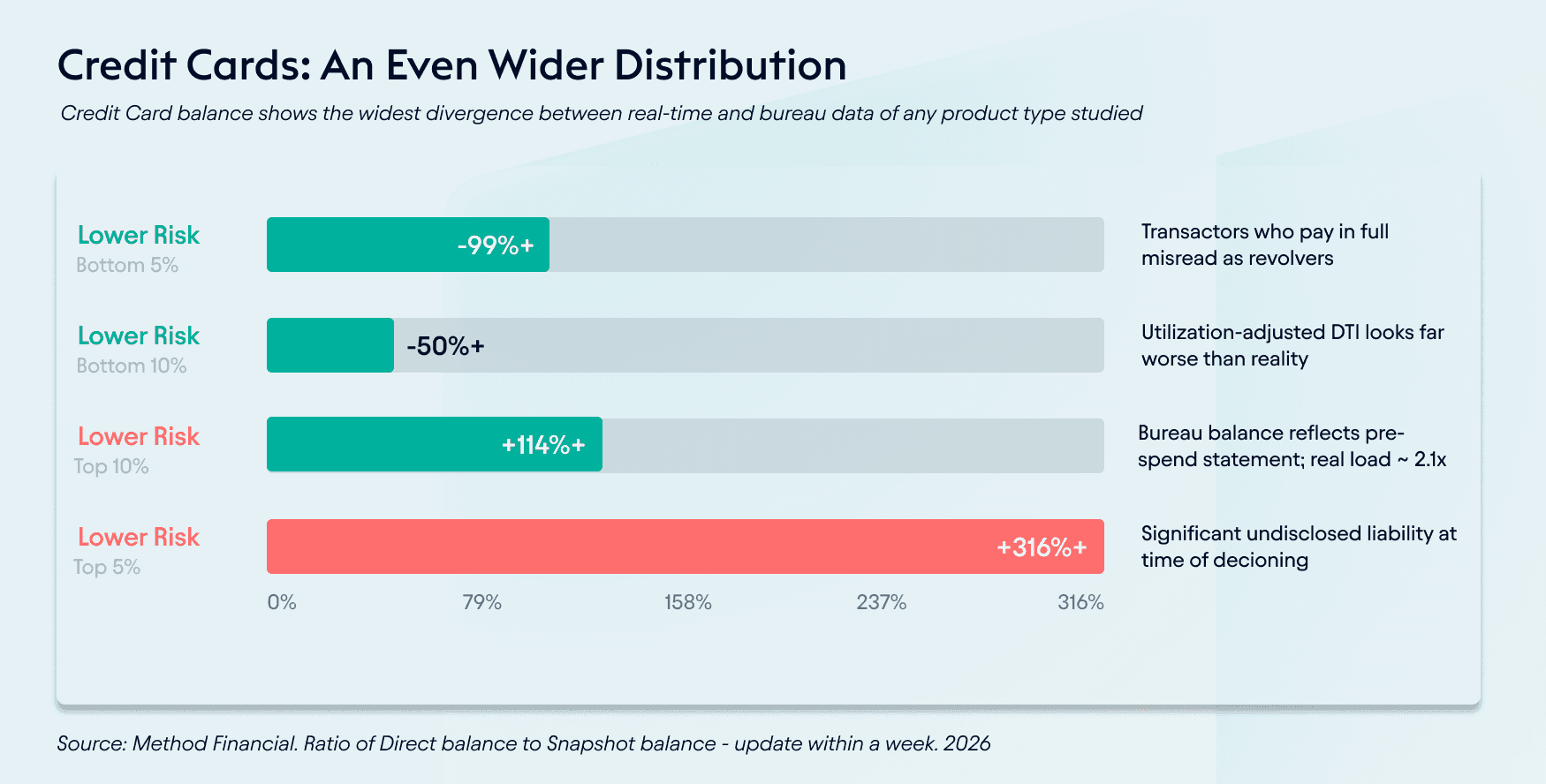

Credit cards exhibit the widest divergence of any product type. This matters particularly for mortgage refinance qualification, where DTI is calculated incorporating all revolving minimum payments. A borrower whose credit card balance appears at $5,000 on the bureau but is actually $11,850 in reality presents a very different DTI than the bureau suggests.

Real-Time Signals as Predictive Indicators

The value of real-time data is not limited to correcting balance inaccuracies. The change in a borrower’s liability profile between bureau reporting cycles contains predictive information about future behavior — information that is only accessible through real-time data streams.

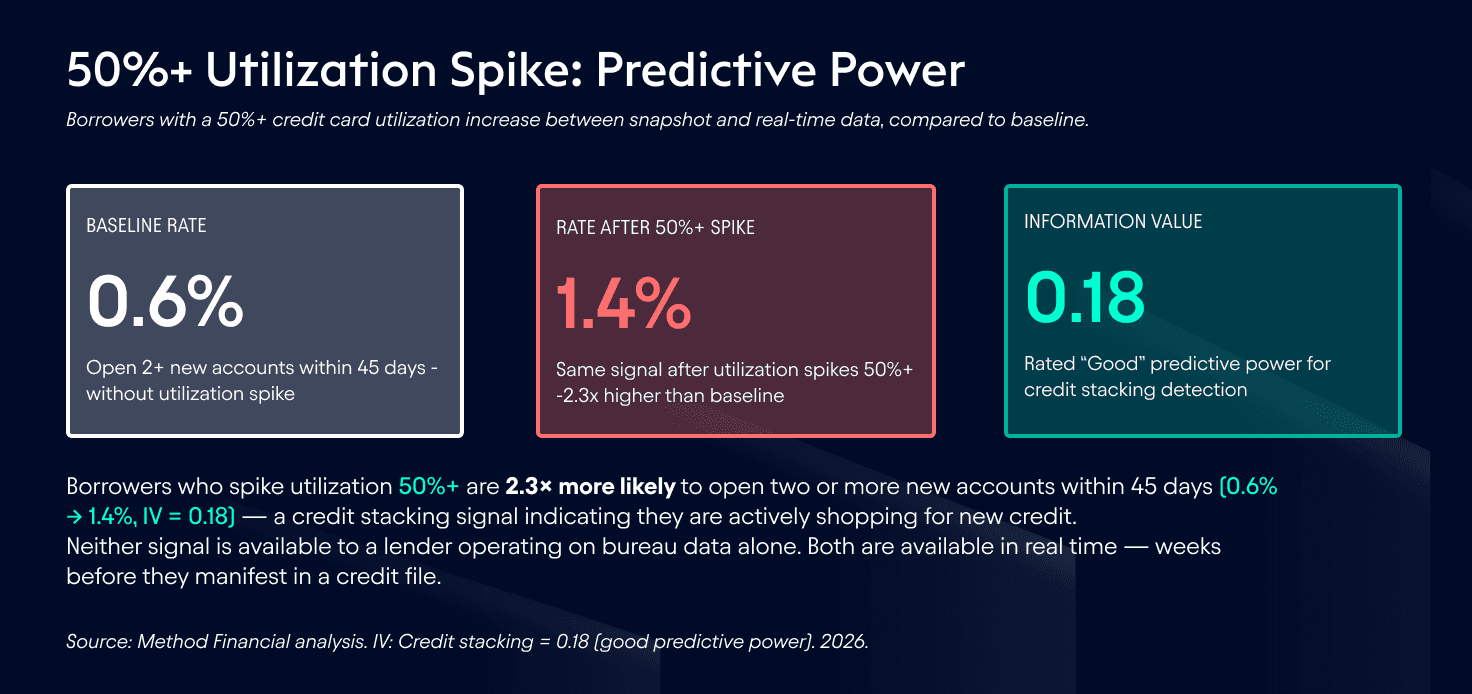

Method’s analysis examined what happens after a borrower’s credit card utilization rises 50% or more between their last bureau snapshot and their current real-time balance — a signal visible in real-time data but invisible to any system relying on bureau pulls.

Borrowers who spike utilization 50%+ are 2.3× more likely to open two or more new accounts within 45 days (0.6% → 1.4%, IV = 0.18) — a credit stacking signal indicating they are actively shopping for new credit.

Neither signal is available to a lender operating on bureau data alone. Both are available in real time — weeks before they manifest in a credit file.

Implications for Refinance Targeting

The consequences of stale liability data manifest differently across mortgage refinance and unsecured personal loan flows — but the underlying distortion is the same: eligibility is being assessed on outdated balance states.

The False Negative Problem in Mortgage Refi

For mortgage lenders, DTI is typically the binding constraint on refinance eligibility. The standard threshold is 45%; the average declined borrower often sits at 46–49%. Among those borrowers, many carry revolving credit card debt that bureau data overstates because the latest statement balance precedes weeks of ongoing payments.

A borrower whose real credit card balance is 29–53% lower than bureau data shows — a condition that applies to 10–15% of personal loan borrowers in Method’s dataset — may present a real DTI of 38–42% while appearing at 47–49% on bureau data. They are eligible. Their bureau file says they are not.

The Timing Problem in Personal Loan Refi

Personal loan originations are at record highs, with much of the growth driven by debt consolidation and credit card refinancing.⁶ The competition for refi-ready borrowers is intense — and the borrowers who are most attractive (consistent paydown, improving utilization) are the ones whose bureau files are most likely to lag their actual financial position.

A 30–45 day head start on the signal means a 30–45 day head start on the offer. In a market where rate windows open and close within weeks, and where consumers actively shop across multiple lenders simultaneously, timing the offer to the actual moment of refi readiness — not to the bureau’s next reporting cycle — is a structural advantage.

The Paydown Velocity Signal

Beyond static balance accuracy, the trajectory of a borrower’s balance is itself a qualifying signal. A borrower reducing their credit card balance by $1,000+ per month for 90 consecutive days is exhibiting deliberate paydown behavior — not seasonal variance. This is observable in real-time data via balance paydown velocity. It is not observable in any bureau file, where only the current balance, not the rate of change, is reported.

The refinance window is increasingly measured in weeks, not quarters. When eligibility models rely on data that lags by 30–60 days, lenders are competing on outdated information.

Liability visibility isn’t just about balance accuracy. It reshapes how lenders identify refinance demand, assess risk, and capture opportunity.

Method gives lenders that real-time edge, turning stale refinance campaigns into smarter, better-timed growth.

METHODOLOGY

Balance staleness analysis is based on Method’s comparison of direct balance reads (pulled within one week of bureau snapshot) against the most recent available bureau snapshot balance, across 14 million U.S. consumer liability records. Direct-to-snapshot ratios are computed at the account level and aggregated by product type and percentile of distribution. Predictive signal analysis (utilization spike → credit stacking / delinquency) uses a 45-day and 6-month forward-looking window respectively, against verified account opening and delinquency flags. Information Value (IV) calculations follow standard credit risk methodology. Data reflects 2025 and 2026 observations.

SOURCES

1. Freddie Mac Primary Mortgage Market Survey (PMMS), February 19, 2026. freddiemac.com/pmms

2. Mortgage Bankers Association, 2026 Mortgage Finance Forecast, October 2025. mba.org

3. Fannie Mae Economic and Strategic Research Group, September 2025 Economic and Housing Outlook. fanniemae.com

4. ICE Mortgage Technology, Mortgage Monitor Report, February 2026. Reported by HousingWire, February 2026.

5. TransUnion Q3 2025 Credit Industry Insights Report; CNBC, “Personal loans surge amid affordability struggles,” February 20, 2026.

6. LendingTree: 35% of personal loan borrowers used proceeds for debt consolidation; 16% for credit card refinancing. TransUnion Q2 2025 CIIR: unsecured personal loan balances hit record $257B.

7. TransUnion 2026 Mortgage & Consumer Credit Forecast. Scotsman Guide, February 2026.