Table of contents

What is Method?

Because Method is a somewhat technical product, we often get questions about what we actually do. People (like you, maybe) wonder what Method is and how it is valuable. In the past, we did not have a useful piece we could point those people to. Now we do—it is the essay you are about to read.

Think of all the people you might meet on a regular day. The barista who makes your morning coffee. Your coworkers. The grocery store cashier after work. The doctor, at your 6pm check-up. The server at dinner.

What one trait do they all have in common?

If you are in the United States, they are probably all in debt. A lot of it. Total consumer debt in the United States is $18.2 trillion. This means the average American adult is $105,000 in debt. Credit cards, student loans, auto loans, personal loans, mortgages. They spend a third of their income every month just paying off debt. Nobody likes talking about it, but debt in the United States is just about everywhere.

It is not just that the average American has debt, but that they lack the tools to effectively manage that debt. Loans stack up across separate platforms. Payments are due at different times of the month. Interest piles up. For many Americans, debt is a problem that gets worse with every month, a problem that continues for generations. Debt is more disconnected and complex than ever, which makes it a mess.

An entire industry of companies has arisen to help you clean up that mess. There are apps that help you monitor your credit. Others that help you earn rewards on your biggest expenses, like Bilt. Companies that help you use your home equity to get out of debt, like Figure. Only it’s much harder than it should be for these companies to do their job. That’s because of something called connectivity.

In order to effectively help you, financial companies need strong and accurate connections to your debt accounts. They need accurate, up-to-date information—like your balance and payment history on a credit card. And they need the ability to take action on your behalf—like scheduling a student loan payment for you. An app designed to help you pay off your debt can’t be useful if it can’t see your debts nor help you make payments on them.

But connectivity is not a solved problem. It has historically been difficult for companies to get your financial data, even with your explicit consent. Instead, companies have to ask you for your login credentials for all your accounts: every credit card, student loan, mortgage that lives across 2,000+ major financial institutions (15,000+ in total). They try to log in (which doesn’t always work). They try to scrape your data (which doesn’t always work). They try to keep this data reliable and up-to-date (which isn’t always possible).

Even when you say “yes, here is my debt information,” companies struggle to get it. And by the time they do, that information has changed.

If someone could build a strong connection to liability accounts, then millions of Americans could finally take control of their debt instead of being controlled by it. And the companies serving them could build entirely new revenue streams around new, useful, consumer credit and personal financial management opportunities.

At Method, we’ve built that connection.

The debt connectivity problem

Before Method, nobody had solved connectivity for liabilities. We found out the hard way.

In 2019, we went through the startup accelerator Y Combinator. We’d founded a company called GradJoy, and the idea was simple: connect all your student loans to GradJoy and we’d make it easy for you to pay them off. It didn’t quite go as planned.

That summer, we were trying to onboard thousands of new students who wanted help paying their loans. One of those students was Sophia: a first-generation college student who had said yes to a sizable loan package when she was 18, before starting her freshman year. There was a new loan assigned for every semester for college, which translates to 8 separate loans to track for an average college graduate.

Years later, out of college and working, Sophia was struggling to pay off her loans. It was hard to tell how much progress she was even making. Sophia knew she was behind, but didn’t know how to change it. And so Sophia downloaded GradJoy.

This is where things started to get complicated. Liabilities are not like bank accounts; they’re fragmented across different lender types and harder to access. One of Sophia’s loan providers (Great Lakes) was niche, so we needed to ask her for her login information and then build complex, brittle workarounds on the backend to pull the data. Another was available through an existing connectivity solution, but the solution broke often. Another wasn’t accessible at all, so we asked Sophia to send us the information in a spreadsheet once per month. Of course, all of this operated on the assumption that Sophia remembered all of her loans (which many students do not).

Once we had her data, we sent Sophia a message. We told her we could help her set up a payment plan, but the lack of connectivity meant we had no way to actually schedule payments on her behalf. She couldn’t just say ‘yes’ to the plan in the app; everything still had to be manual.

And so, from Sophia’s perspective, the situation was still a mess. She didn’t have comprehensive and reliable data about her liabilities in one place. She still couldn’t automate payments to make sure she stayed on track. It was bad for us at GradJoy, too, because the lack of connectivity made it difficult for us to be useful. Nothing was automatic. Nothing was smooth. Everything was fragile, tedious, and broken.

This wasn’t just the status quo for us at GradJoy. It is the status quo—for everyone. From the small GradJoys of the world to leading financial institutions like Credit Karma.

Now, you may be wondering: Why hasn’t anybody fixed this?

Prior attempts to solve connectivity with APIs

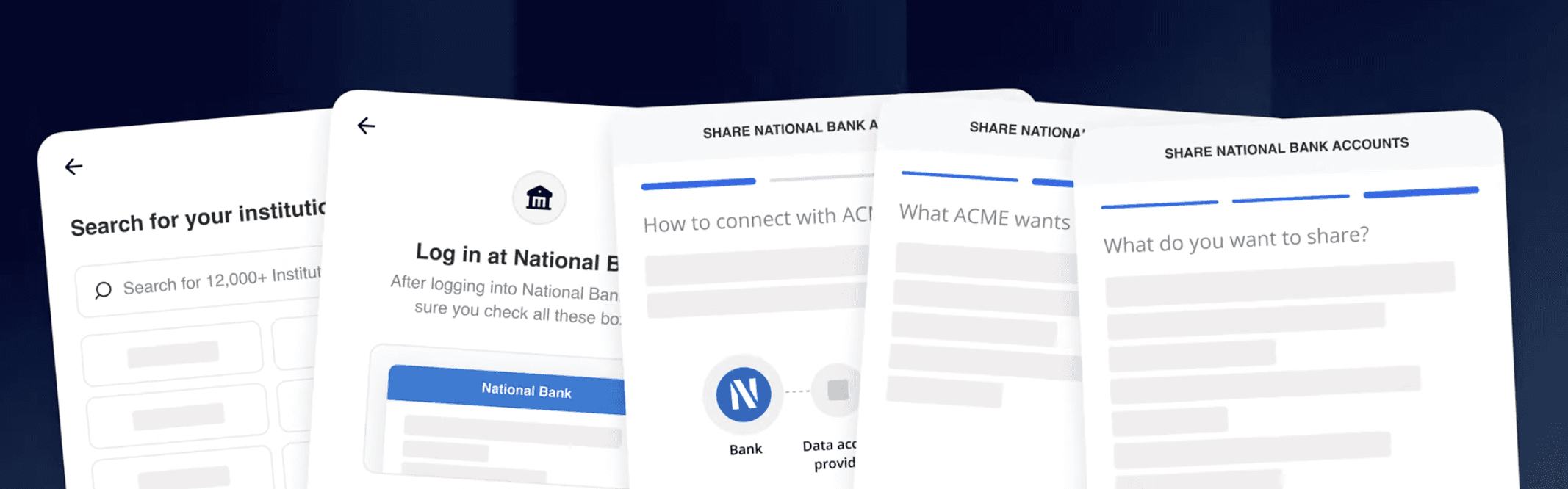

The process for building a connectivity product is straightforward: (1) build some underlying solution that makes the connection, and then (2) provide access to that product via an API; an app for apps. This lets others, like a personal finance app, plug into a user’s data with a few lines of code.

If you’ve ever seen screens like this, you’ve probably interacted with a financial connectivity API.

Thus far, companies have done a decent job at solving some connectivity problems, like bank accounts. That’s because bank accounts follow a standard: they have routing numbers, shared protocols, and are governed by common infrastructure. But liabilities are more fragmented, more variable. Even within one financial institution, there may be thousands of different permutations of liabilities and the way those account details are reported.

This complexity is why the liability problem has remained mostly unsolved. And the few solutions that do exist today often use ineffective tactics under the hood:

They require users to put in their username and password (which means fewer people do it).

They pull outdated credit report data.

They use unreliable tactics (like screen scraping).

They fail often, with connection rates sometimes below 50%.

Users have to connect their accounts one-by-one, which is tedious (and users can forget things).

The data is not refreshed and can often be 30+ days old, which makes it unhelpful.

Not all existing financial connectivity APIs can facilitate payments.

You can see the problem. It’s hard to be useful to users if you can’t always connect to their liability accounts, and if the connections you can make are unreliable. The way you unlock real opportunity is by having smooth, frictionless, reliable connectivity that isn’t a burden on the user.

That connectivity is exactly what Method provides.

What we’ve built and why it matters

When a company is using Method’s API, the end-user (you!) often does not even notice. You sign up as normal to any app: by giving it your name and phone number. That app then passes Method your information, and Method works its magic.

In seconds, you can choose which liability accounts you’d like to connect to whatever service or app you’re using. Once your accounts are connected, payment functionality can also be turned on; this means that you could, for example, pay off your credit cards directly from your personal finance app.

If you are reading this, it’s unlikely that you are quite as obsessed with financial connectivity APIs as we have been over the past few years. At least you aren’t yet. But the way Method works is new to the industry. We are the first API that makes connectivity this simple and reliable, which explains our early success so far. Our new approach creates opportunities for both financial companies and regular people.

Bilt uses Method to increase the average number of credit cards a user connects by 2.5x.

SoFi uses Method to expand personal loan coverage for pay off by 78%.

Cleo uses Method to display rich liability insights to its millions users.

As Method continues to grow, we have a few predictions around what will happen.

People will spend less money on debt. This is partly because they’ll have a more clear understanding of their financial picture and partly because Method enables financial services to become more effective at helping people pay their debt. This alone is a big step forward in a country plagued by consumer debt.

Related, financial services will become dramatically more efficient and helpful. Your finance app, or credit score website, or credit card company can help you better when they know more about your financial picture. This also unlocks ways for them to invent new revenue lines by making themselves more useful to customers in ways that would have been impossible without Method-level connectivity.

Broadly, we believe that everyday people—especially people who were previously underserved—will have more financial literacy and agency, and less stress. People will know what’s going on, and it will be easier than ever for them to figure out paths to take control over their debt and their financial future.

To us, this is an optimistic picture of the future. And, if things work out, Method will be at the center of it all.

If you’d like to help us build Method

You may have some questions about Method as a company. The short answer is that, while we have a long way to go, so far we have seen success. We’ve processed over $2.5B in payments. One in every three credit cards in the United States is in the Method ecosystem. Leading financial institutions like SoFi and Bilt rely on our APIs to build magical experiences for hundreds of millions of consumers. And last year, we raised a $42M Series B led by Emergence Capital and Andreessen Horowitz.

But Method is not a huge company. For instance, our engineering team is just 8 people. When candidates come to interview with us in person, they tend to be surprised by this. The truth is, we are small not because the product is easy to build, but because we’re all interdisciplinary. Our accounting team knows APIs and our sales team jumps into Figma to mock up experiences.

Of course, we sometimes do need to hire people, and if you have made it this far in the essay perhaps you’d like to chat about working with us.

If working at Method seems interesting to you, drop me a note: jose@methodfi.com

Or, if you want to explore how real-time connectivity can transform your business, book a demo here.