Perspectives

Improve Debt Consolidation Performance with Repayment Certainty

Jose Bethancourt

Co-founder & CEO

Table of contents

Leverage Method's Direct Pay to offer APR discounts and assess borrower eligibility with repayment certainty. Gain confirmation an applicant will pay off loan balances right from the application flow before a loan is approved and automate direct debt payments. Method helps lenders boost revenue and profits by:

Increasing borrower eligibility with changing credit policy

Approving larger loans at scale

Speeding up utilization

Decreasing default rates

Improving borrowers' financial outcomes

Here's an example Personal Loan application that incorporates Method's embedded repayment experience as part of pre-qualification.

Better Risk Assessment with No Credit Policy Change

Extend debt to more qualified borrowers by integrating Method directly into the application flow. Ask applicants to select the debt they want to pay off before calculating their DTI (debt-to-income) ratio. If an applicant agrees to pay off debt, their DTI drops, increasing the likelihood that the loan will be approved. Lenders can repay creditors directly with Method, once the loan is issued.

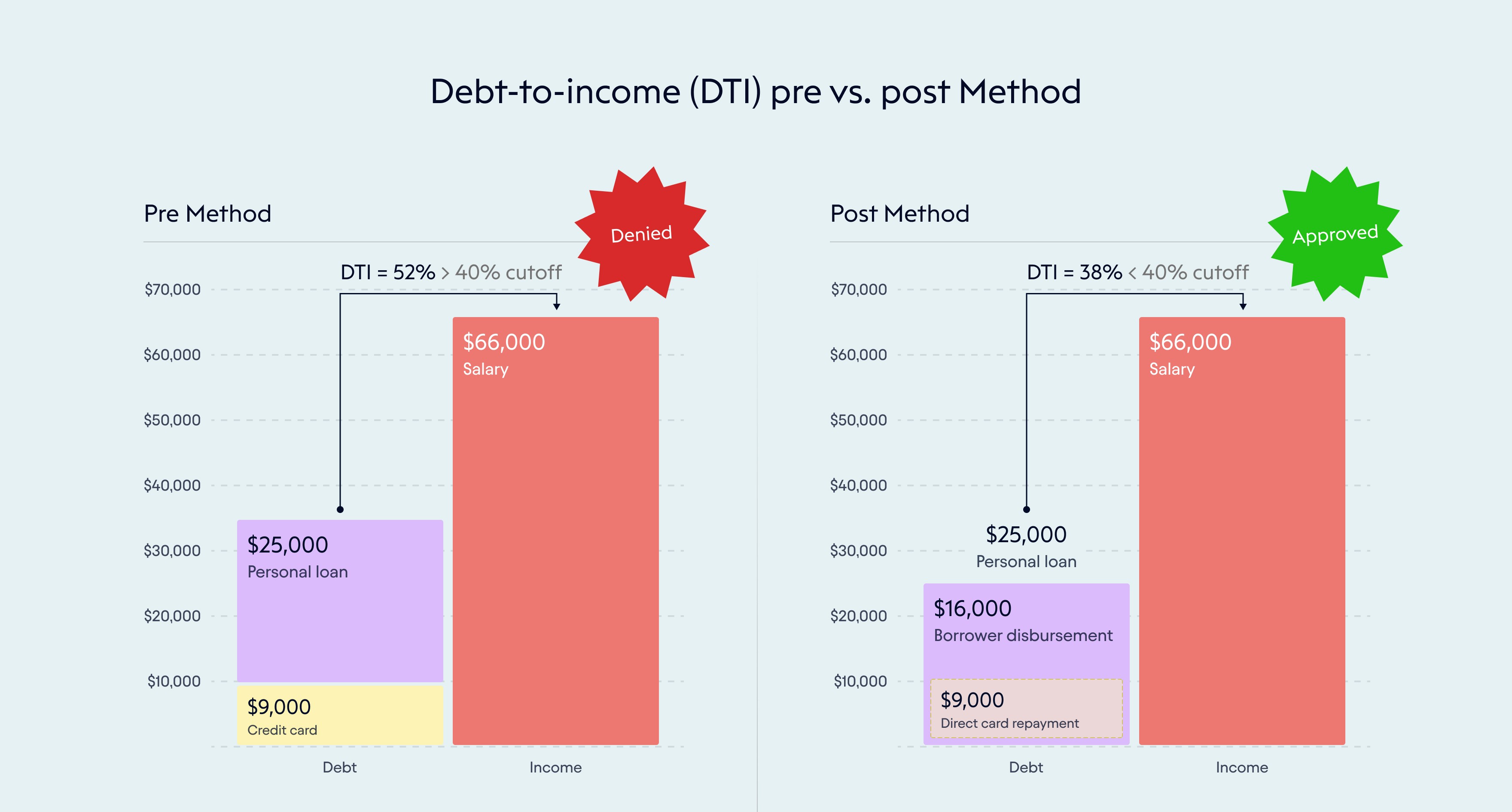

Here’s a simplistic example that brings home the point:

A consumer applies for a $25,000 personal loan. They earn an annual salary of $66,000 and have $9,000 in outstanding credit card debt. Old debts are added to new debts and the applicant’s DTI is calculated as $34,000 / $66,000 or 52%. That’s above the lender’s cap of 40%. The loan is denied.

That same consumer applies for a loan with a lender that has integrated Method into its application flow. The lender asks if the applicant wants to pay off their credit card debt with a portion of their loan proceeds. The applicant agrees. Their DTI is now calculated at $25,000 / $66,000 or 38%. The loan is approved (assuming their DTI ceiling is 40%). The lender uses Method to pay off the debt with the loan proceeds.

Reduce an applicant’s DTI by factoring debt payoff commitments into the calculation.

Approve Larger Loans at Scale

Customers using Method’s payment rails report that borrowers increase the average repayment amount by 25%. If Method is integrated directly into the application flow, lenders can safely originate larger loans without increasing the default rate.

This applies whether a borrower applies online or in a branch. Today, several online lenders meet with approved applicants in person to gain repayment commitments before disbursing funds. These lenders may offer larger loan amounts if an applicant agrees. But this process isn’t scalable given that the lender does this on the back-end as an added step. Plus, it requires the lender to set up a repayment processing center.

With Method payment rails, loan officers can immediately process debt repayments and issue larger loans at scale. Imagine a borrower needs a $10,000 loan but only qualifies for a $5,000 loan. The lender can’t access payment rails and therefore can’t issue the larger loan. With Method, a loan officer can pay off that borrower’s other debts in seconds and increase the loan value to $10,000.

Speed up Utilization and Additional Revenue Streams

HELOCs and Balance Transfer cards often allow borrowers to spend or utilize funds as needed. When some or all of a loan’s proceeds are immediately used to pay down debt, borrowers utilize their credit line more quickly. HELOC lenders typically see full line utilization around 40 days, but with repayment certainty, line utilization begins as soon as the HELOC is approved. Additionally, lenders are able to generate higher revenue through balance transfer fees. Payments with Method settle in 1-3 business days with coverage across 20k FIs. Accounts are confirmed payable before being surfaced to the borrower during their no-impact rate check.

Reduce Default Rates and Improve Capital Markets Performance

Lower the average DTI of a loan portfolio by adding debt repayment guarantees to the application flow. This will reduce default rates given the clear, positive correlation between the two. Lenders like Figure have seen a 50 decrease in 60-day delinquencies for Direct Pay borrowers and better performance on secondary markers.

Drive Better Borrower Outcomes

Figure's Direct Pay borrowers lowered monthly payments by 504% and improved their FICO scores by 21.6 points, leading to 50% increase in follow-on lending and improved LTV.

Conclusion

Repayment certainty directly translates into improved debt consolidation performance. Method helps lenders unlock revenue growth, reduce risk and deliver a better customer experience.