Method Labs

Follow the Money: What Direct Pay Means for Lenders

Artem Vasilkovskiy

Director, Strategy & Growth

Priyanshi Churiwala

Product Lead, Lending

Table of contents

How Direct Pay turns intent into outcome

Unsecured personal lending is accelerating. Through December 2025, new personal loan originations totaled $75.2 billion, up 17% year-over-year¹. In a separate survey of prospective borrowers, 57% cited debt consolidation as their primary reason for considering a personal loan — the single most common stated use case².

Underwriting these loans is complex, given limited insight into how funds are ultimately used and the typical lack of collateral.

With cash disbursement, the lender’s visibility ends at funding. Did the money go to the named creditor or somewhere else entirely? In most cases, lenders don’t know whether the consolidation actually happened until bureau data refreshes roughly 22-37 days later. By then, the borrower may be carrying two full debt loads — the new installment loan on top of the unretired revolving balances.

Direct Pay closes that gap. Instead of wiring proceeds to the borrower’s bank account, funds go directly to the target creditors at funding. Balances are settled at the source and lenders can track payment status from initiation through posting.

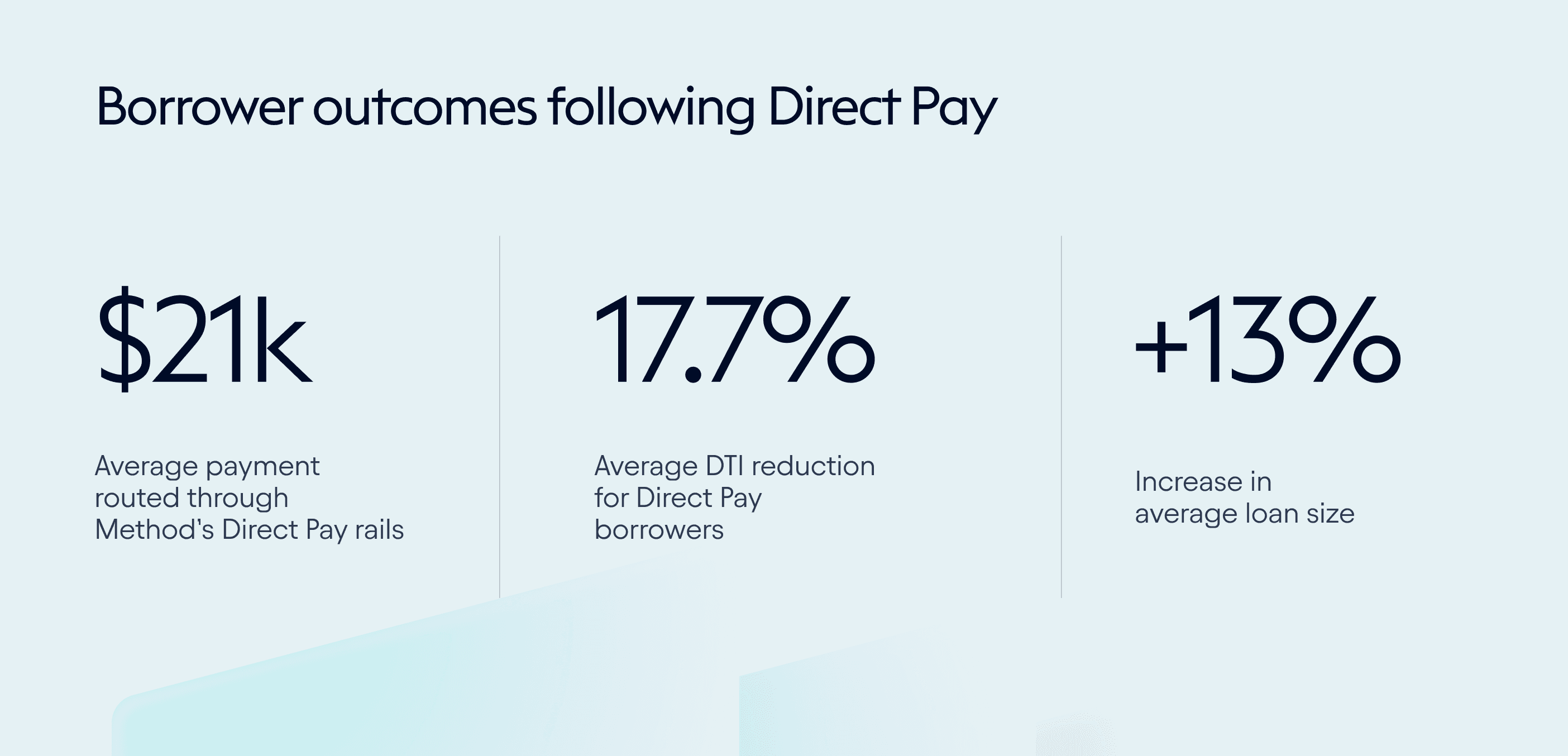

Here’s what Direct Pay with Method actually delivers, based on the data of tens of thousands of borrowers.

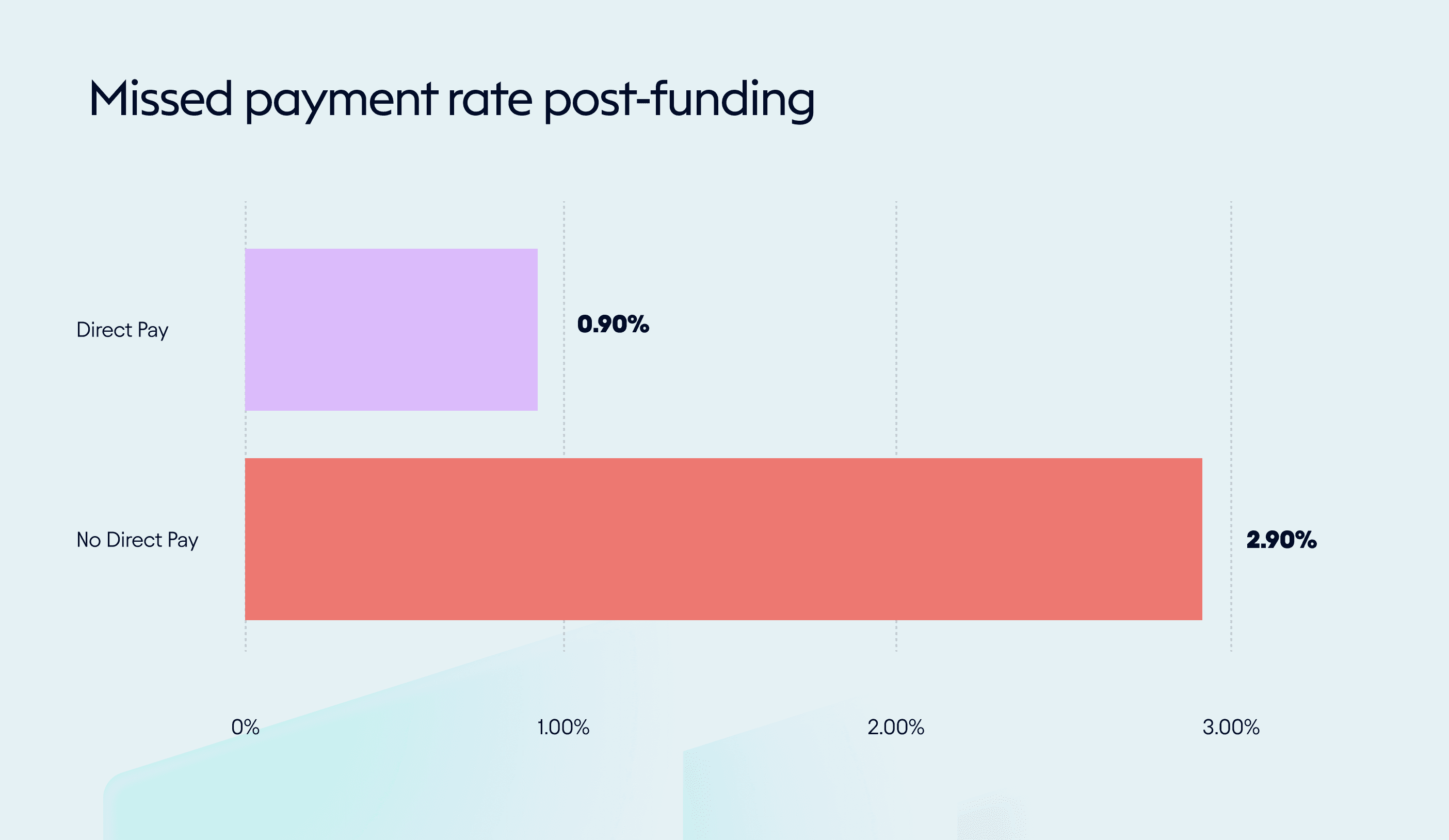

Finding 1: Delinquency rates diverge

Borrowers who had their debt paid down at funding were less likely to miss a payment in the two months that followed. We tracked more than 36,000 borrowers, comparing those whose debt was paid at funding against a matched group that had not. Both groups were on the same platforms over the same two-month period, matched on risk profile at origination.

The Direct Pay group showed significantly lower delinquency rates than the matched non-direct-pay cohort. The payoff itself is doing something — not just the type of borrower who opts into it. Direct Pay borrowers begin repayment with lower revolving utilization and fewer obligations competing for the same cash flow.

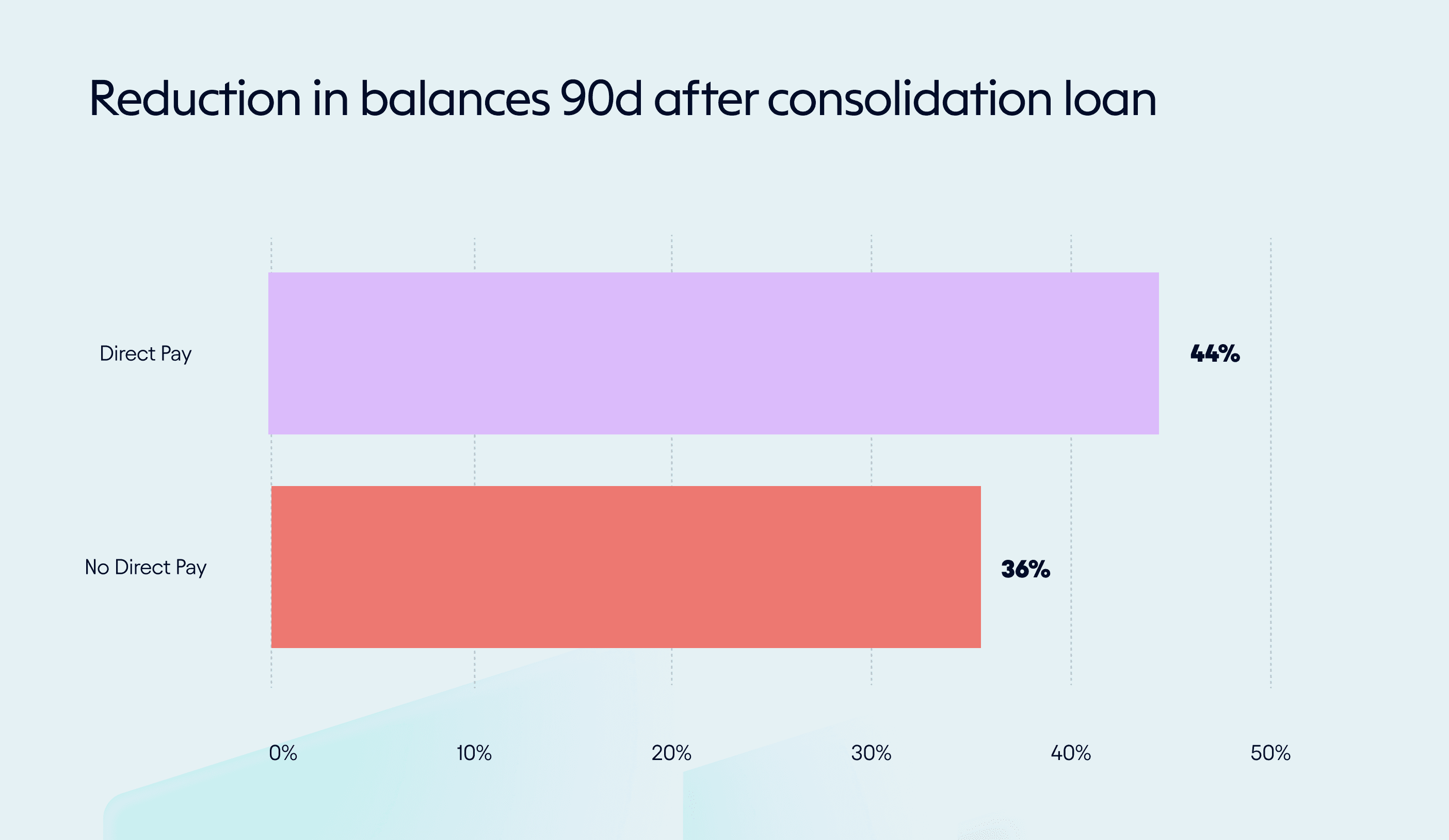

Finding 2: The paydown sticks

A common concern with consolidation products is that borrowers pay down their debt and then quickly reload it. We measured how total personal loan and credit card debt changed 60–90 days after consolidation loan origination for accounts that existed prior to consolidation.

Direct Pay borrowers reduced their balances by 44% — compared to 36% for borrowers without Direct Pay. The 8% gap reflects the efficiency of the mechanism: when loan proceeds go directly to creditors, the debt is actually retired rather than redirected.

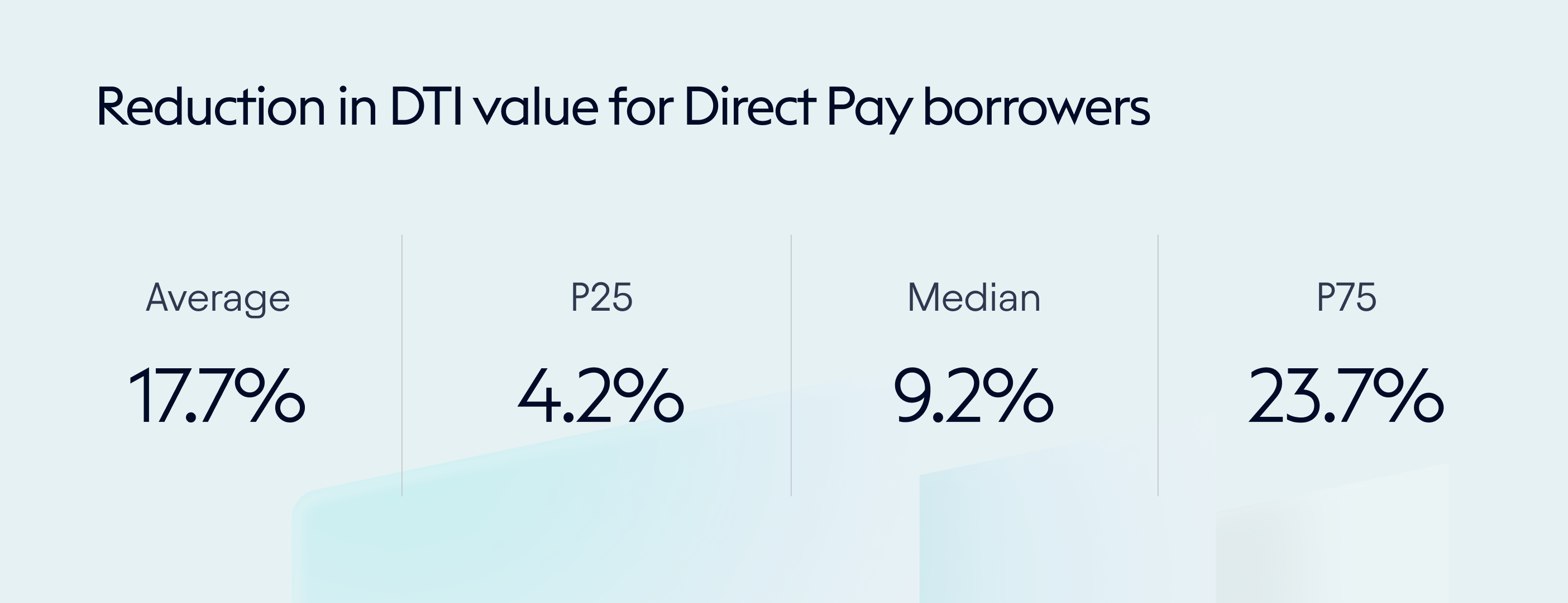

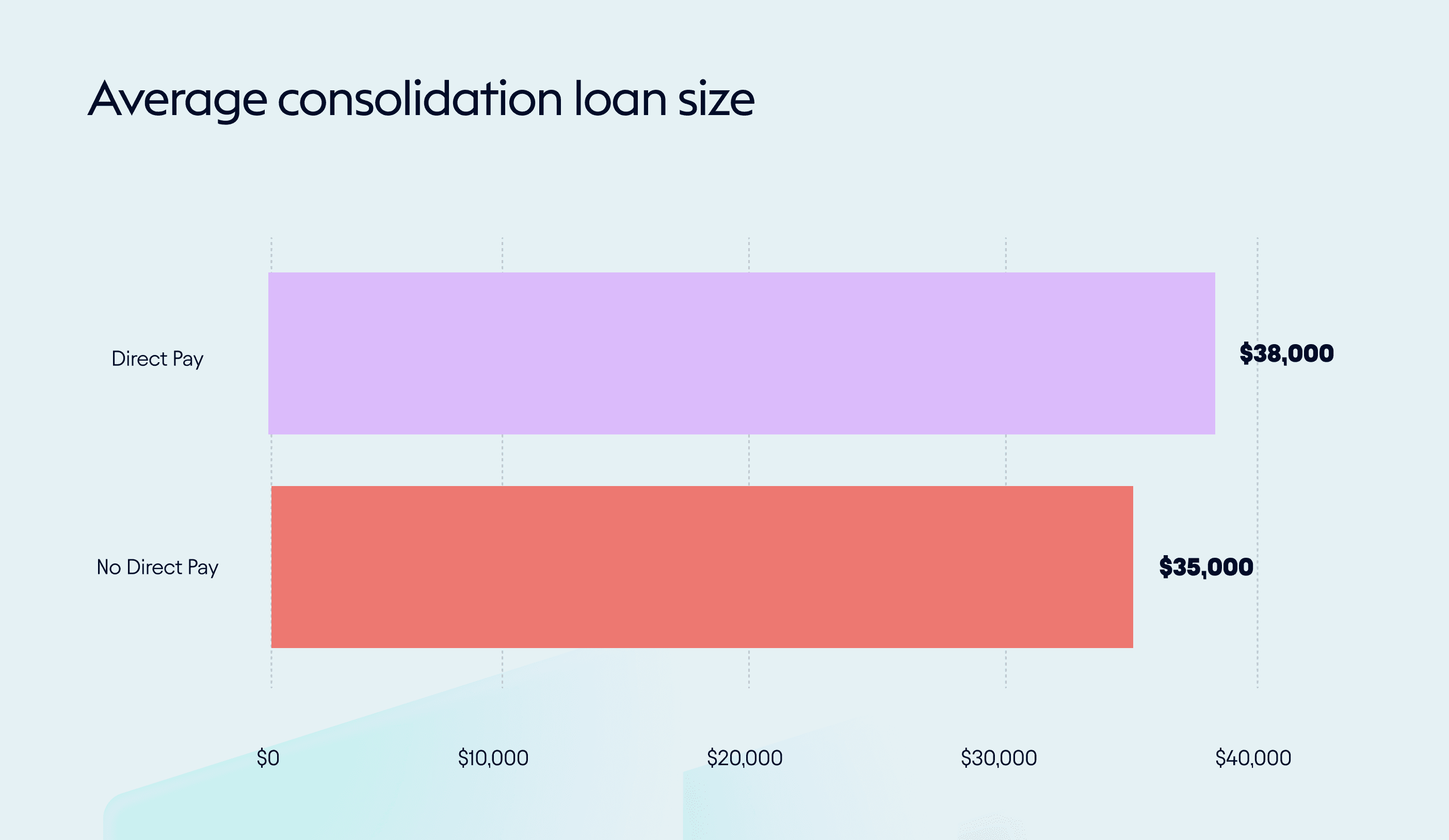

Finding 3: Better borrower profiles unlock larger loans

Take two borrowers consolidating debt. They came in through the same product and for the same purpose. What differed was what happened to the loan proceeds.

If the money goes directly to the creditor that is reflected in DTI: Direct Pay borrowers saw an average 17.7% reduction, with the heaviest borrowers seeing nearly 24 points come off.

A 17.7% DTI reduction is the difference between qualifying and not qualifying, or between a $35,000 loan and a $38,000 one — which is exactly what we see in our data.

What this looks like in practice

Figure, the largest non-bank HELOC originator, engineered their product around this exact mechanic. Borrowers select which debts to pay off at close, Method routes proceeds directly to each creditor at funding, and Figure applies the DTI credit at underwriting, not on stated intent.

The results were telling: 11% higher loan value, 50% lower 60-day delinquency rates.

Conclusion

Portfolio growth and risk reduction almost never move in the same direction. Lenders who want more volume typically accept more risk to get it. Lenders who want a cleaner book pull back on approvals.

Direct Pay sidesteps that trade-off. When existing debt is retired at funding, DTI improves, outstanding obligations fall, and repayment capacity strengthens. The same product, offered to the same borrowers, produces a larger book and a better-performing one. No change to the credit box. No change to the target customer. Just a different answer to the question of where the proceeds go.

Intent to consolidate isn't a repayment strategy. Verified payoff is. If you want to learn what Direct Pay would look like for your organization, book a demo here.

Explore how lenders are using Direct Pay today:

REFERENCES

¹ Consumer Pulse: The Latest Consumer Credit Trends, April 2026, Equifax

² Most Americans Considering Personal Loans Are Focused on Debt Reduction, Not Spending, February 2026, SoFi

Method Financial. (2026). Direct Pay Outcome Study. N = 36,000 borrowers.

Method Financial. (2026, Q1). Post-Payment Credit Behavior Analysis: Missed Payments, Balance Paydown, and New Account Origination. N = 30,000 borrowers.